Introduction

As a DSA agent, mastering business loan basics for DSAs is essential. Moreover, business loans offer higher commission rates compared to personal loans. Therefore, understanding this product boosts your income significantly.

Furthermore, many entrepreneurs need business loans for growth and expansion. Additionally, the business loan market is growing rapidly in India. Consequently, opportunities for DSAs are expanding every day.

In this guide, we’ll cover the basic idea of business loans for DSA agents. Moreover, you’ll learn about types, eligibility, documentation, and selling strategies. By the end, you’ll confidently pitch business loans to customers.

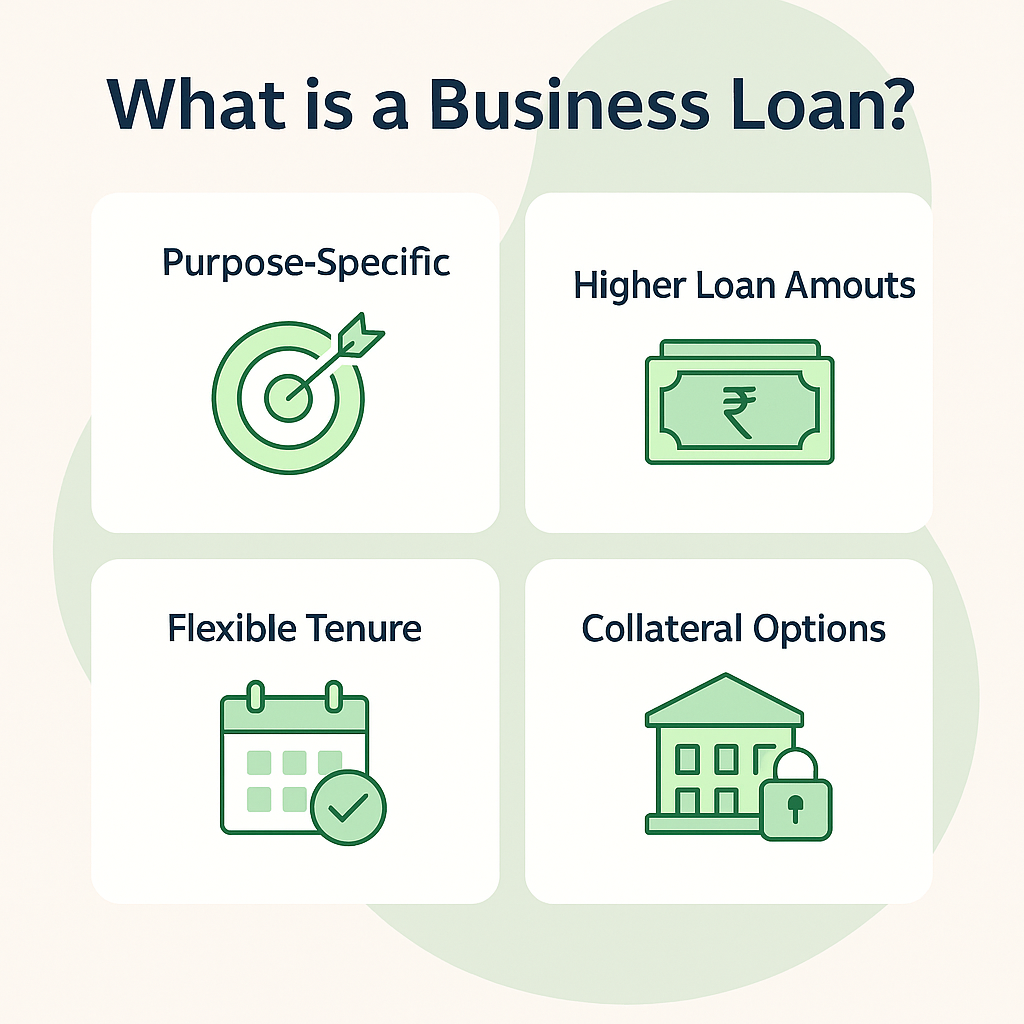

What is a Business Loan?

Let’s start with the basic question: what exactly is a business loan?

Definition

A business loan is a credit provided to entrepreneurs for business purposes. Moreover, it helps fund operations, expansion, equipment, or working capital. Therefore, it’s specifically designed for business needs, not personal use.

Key Characteristics

- Purpose-Specific: Business loans must be used for business activities only. Therefore, lenders verify the purpose before approval.

- Higher Loan Amounts: Business loans range from Rs. 50,000 to Rs. 50 crores. Therefore, they suit businesses of all sizes. Moreover, amounts depend on business revenue and requirements.

- Flexible Tenure: Repayment periods vary from 1 to 10 years. Also, some lenders offer customized tenures.

- Collateral Options: Business loans can be secured or unsecured. Moreover, secured loans offer higher amounts and lower rates. However, the unsecured loan process is faster.

Why Businesses Need Loans

- Working Capital: To manage daily operational expenses.

- Expansion: For opening new branches or entering new markets.

- Equipment Purchase: To buy machinery, vehicles, or technology.

- Inventory Management: To stock products during peak seasons.

- Business Establishment: To start new ventures or businesses.

Types of Business Loans

Understanding different types of business loans helps you match customers with relevant products. And, this increases your conversion rates significantly.

Based on Security

- Secured Business Loans: These require collateral like property or machinery. Moreover, they offer higher amounts and lower interest rates. Therefore, they suit established businesses with assets.

- Unsecured Business Loans: These don’t need collateral. However, interest rates are slightly higher. Therefore, they’re perfect for businesses without significant assets.

Based on Purpose

- Working Capital Loans: For daily operational needs like salaries and rent. Moreover, they have shorter tenures, typically 1-3 years. Therefore, they help manage cash flow gaps.

- Term Loans: For long-term business needs like expansion. They come with longer repayment periods. Therefore, they suit major business investments.

- Equipment Financing: Particularly for purchasing machinery or equipment. Moreover, the equipment itself serves as collateral.

- Invoice Financing: Against pending customer invoices. Additionally, businesses get immediate cash. Therefore, it solves payment delay issues.

- Loan Against Property (LAP): Using business property as security. Moreover, it offers the highest loan amounts. Therefore, it’s ideal for major expansions.

Business Loan Eligibility Criteria

Knowing eligibility helps you identify qualified customers quickly. Moreover, this forms the core of business loan basics for DSAs.

Standard Eligibility Requirements

| Criteria | Requirements | Why It Matters |

| Business Vintage | 1-3 years minimum | Proves business stability |

| Annual Turnover | Rs. 10 lakhs+ | Shows business capacity |

| Age | 21-65 years | Legal and working capability |

| Credit Score | 650+ (700+ preferred) | Financial reliability |

| Business Type | Registered entity | Legal compliance |

| Profitability | Positive last 2 years | Repayment capacity |

For Proprietorships

Individual business owners need:

- Minimum 2 years of business existence

- Consistent income proof

- Personal and business documents

- Good personal credit score

For Partnership Firms

Partners collectively need:

- Partnership deed

- All partners’ documents

- Business registration proof

- Minimum 3 years of operation of the company

For Private Limited Companies

Corporate entities need:

- Certificate of incorporation

- Board resolution for a loan

- Company financial statements

- Directors’ personal guarantees

Therefore, companies have formal requirements.

Documents Required

Proper documentation is required for business loan approval. Moreover, complete paperwork speeds up processing significantly.

- Business Documents

1. Registration Proof:

- Business registration certificate

- GST registration

- Shop and establishment license

- Partnership deed (if applicable)

2. Financial Documents:

- Last 2-3 years’ IT returns

- Audited financial statements

- Bank statements (12 months)

- Profit and loss statements

3. Business Proof:

- Business address proof

- Rent agreement (if applicable)

- Utility bills

- Customer contracts

- Personal Documents

1. Identity Proof:

- PAN Card (mandatory)

- Aadhaar Card

- Passport

- Voter ID

2. Address Proof:

- Aadhaar Card

- Utility bills

- Rent agreement

- Passport

Hence, both business and personal documents are essential.

How Business Loans Work

Understanding the process helps you guide customers effectively. Moreover, this knowledge separates average DSAs from top performers.

Application to Disbursal Process

- Step 1: Business Assessment

First, evaluate the customer’s business viability. Moreover, check if they meet basic eligibility criteria.

- Step 2: Documentation

Next, help customers gather all required documents. Moreover, ensure everything is complete and accurate.

- Step 3: Lender Selection

Then, choose the right lender for the customer’s profile. Moreover, consider interest rates and processing time.

- Step 4: Application Submission

After that, submit the complete application with documents. Moreover, most lenders now accept online submissions.

- Step 5: Verification

Later, lenders verify business and financial details. Moreover, they may visit the business premises.

- Step 6: Approval

Once the above processes are satisfied, lenders approve the loan with terms. And, they communicate the amount, rate, and tenure.

- Step 7: Agreement Signing

Finally, customers sign the loan agreement. Moreover, this can happen digitally now.

- Step 8: Disbursal

The loan amount gets credited to the business account. Moreover, this typically takes 5-10 days from approval. Therefore, plan accordingly.

Interest Rates and Charges

Business loan interest rates range from 12% to 24% annually. Moreover, rates depend on:

- Business vintage and stability

- Annual turnover

- Credit score

- Collateral (if any)

Also, lenders charge processing fees of 1-3%. Therefore, factor this into customer discussions.

Why Choose to Sell WeRize Business Loan?

The WeRize Business Loan offers a seamless financing solution tailored for business owners and self-employed individuals looking to grow their business.

With a completely digital application process, it allows fast approval and easy access to funds, even for those with no prior loan history. DSAs can help customers benefit from this opportunity while earning attractive commissions on every successful loan disbursal.

By referring qualified business owners, you not only help them expand but also boost your own income. It’s a smart and rewarding way to unlock financial growth.

Tips for Selling Business Loans

Here are practical strategies based on business loan basics for DSAs.

Identify Potential Customers

Who Needs Business Loans:

- Businesses planning expansion

- New entrepreneurs requiring capital

- Seasonal businesses requiring inventory funding

- Businesses facing cash flow issues

Qualification Questions

Before proceeding, ask:

- How long has the business been operating?

- What’s the annual turnover?

- What’s the loan purpose?

- Is the business registered?

- Are financial records maintained?

Building Trust

- Understand Their Business: Show genuine interest in their operations. Moreover, ask about their challenges and goals.

- Speak Their Language: Use business terms properly. And, demonstrate industry knowledge. Therefore, customers trust your expertise.

- Be Transparent: Explain all terms, rates, and charges clearly. Moreover, don’t hide any information.

Conclusion

Mastering business loan basics for DSAs opens considerable earning opportunities. As it’s covered, business loans are complex but rewarding products. Moreover, they offer higher commissions and help you build valuable business relationships.

Furthermore, remember that every business has unique needs. Therefore, customize your approach for each customer. Moreover, continuous learning about different industries helps you serve better.

Additionally, don’t get discouraged by rejections. Instead, learn from each application.

So, use this basic idea on a business loan for a DSA work to start selling confidently. Moreover, keep updating your knowledge as products evolve.

Ready to sell business loans? Apply these fundamentals with your next entrepreneur customer today!

Frequently Asked Questions

Q1: What are the business loan basics for DSAs?

Business loan basics for DSAs include understanding loan types, eligibility criteria, documentation requirements, and selling strategies. Moreover, it covers how business loans differ from personal loans.

Q2: How is a business loan different from a personal loan?

Business loans are for business purposes only, with higher amounts and longer tenures. Moreover, they require business documents and proof of operations. Therefore, the approval process is more detailed than for personal loans.

Q3: What commission do DSAs earn on business loans?

Commission typically ranges from 1-3% of the loan amount. However, some lenders offer up to 4% on larger loans. Therefore, business loans can earn you Rs. 10,000-50,000 per case.

Q4: What’s the minimum business vintage required?

Most lenders require 1-3 years of business operations.

Q5: Can a new business get a loan?

Yes, but options are limited. Moreover, they need strong business plans and personal guarantees. Therefore, established businesses have better chances and terms.

Q6: What documents are most important for business loans?

GST registration, IT returns, and bank statements are crucial. Moreover, business registration proof is mandatory.

Q7: How long does business loan approval take?

Typically, 7-15 days from complete application. However, some fintech lenders approve within 48 hours. Therefore, processing time varies by lender.

Q8: Can businesses get unsecured loans?

Yes, unsecured business loans are available up to Rs. 25-30 lakhs. However, they require strong business credentials. Therefore, newer businesses might need collateral.

Q9: What if the business doesn’t have all the documents?

Work with the customer to obtain missing documents. Moreover, some alternative lenders have flexible requirements.

Q10: How can DSAs increase business loan conversions?

Understand the customer’s business thoroughly. Moreover, choose the right lender for their profile. Additionally, prepare complete documentation upfront

{kind=link}